The Current State of Agricultural Financing: Structural Gaps and Systemic Risks in Emerging Markets

Introduction: A System That Expands but Does Not Evolve

Agricultural finance in emerging markets has expanded significantly over the past decades. Governments, development institutions, and financial systems have all increased their focus on the sector.

Yet despite this expansion, the system has not fundamentally evolved.

Access to credit remains uneven. Risk is inconsistently assessed. Financial institutions remain cautious. Farmers continue to rely on informal or suboptimal financing channels.

The issue is not the absence of capital. It is the persistence of structural inefficiencies in how agricultural risk is understood and managed.

This gap defines the current state of agricultural financing.

The Structural Gap: Demand Far Exceeds Effective Supply

Agriculture in emerging markets is dominated by smallholder farmers who operate under constrained conditions.

These farmers typically face:

- limited or no formal credit history

- lack of legally enforceable collateral

- seasonal and volatile income patterns

- geographic and infrastructural limitations

Financial institutions respond rationally by restricting exposure. Lending is concentrated among borrowers who meet formal requirements, leaving a large portion of productive farmers underserved.

This creates a systemic imbalance:

- high demand for financing

- limited effective supply

- inefficient capital allocation

The result is not just exclusion, but misallocation of financial resources at scale.

Collateral-Based Lending: A Structural Constraint

Collateral remains the dominant mechanism for managing credit risk in agriculture.

Land, when formally titled, serves as the primary security. In some cases, equipment or stored commodities are used.

However, collateral introduces several structural limitations:

- It excludes farmers without formal assets

- It provides limited insight into repayment capacity

- It does not capture production or operational risk

- It is difficult to enforce in practice

Collateral reduces loss given default, but it does not prevent default.

In agricultural systems, where risk is driven by weather, management, and market conditions, collateral creates a false sense of security while leaving the core risk drivers unaddressed.

Information Asymmetry: The Central Constraint

The most critical weakness in agricultural finance is the lack of reliable, structured information.

Lenders typically have limited visibility into:

- farm productivity and yield potential

- farmer capability and management practices

- environmental and climate exposure

- real-time crop conditions

This creates information asymmetry between the borrower and the lender. The consequences are predictable:

- conservative lending behavior

- mispricing of risk

- adverse selection

High-quality borrowers are often excluded, while risk is not effectively differentiated across the portfolio.

Climate Risk: A Systemic Variable That Remains Underpriced

Agriculture is inherently exposed to climate variability, yet climate risk remains insufficiently integrated into most credit models. In many emerging markets:

- Weather shocks are frequent and severe

- Insurance penetration is limited

- Credit assessments rely on historical data

This creates a structural mismatch between forward-looking risk and backward-looking models. As a result:

- systemic risk accumulates within portfolios

- volatility increases over time

- lending cycles become unstable

Climate risk is not an external factor. It is a core determinant of repayment capacity.

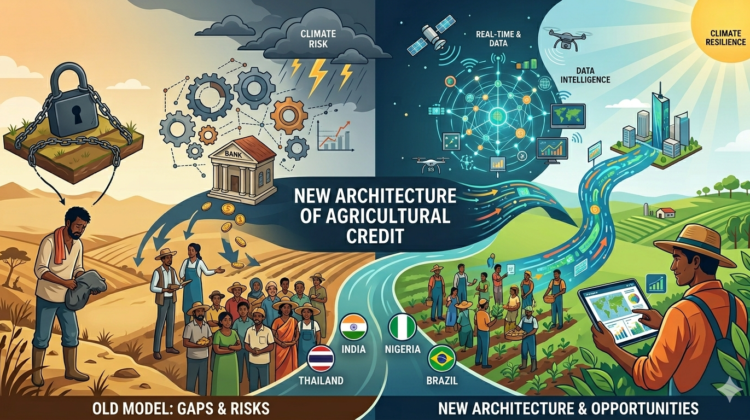

Global Paradigms: Case Studies in Agricultural Credit

Different countries have developed distinct approaches to agricultural financing. These models reflect institutional structures, policy priorities, and risk tolerance.

India: Scale Through Policy-Driven Credit Expansion

India has built a large agricultural credit system supported by priority sector lending mandates. This has enabled significant credit flow to farmers, including smallholders. However, credit allocation is often influenced by policy targets rather than granular risk assessment. This leads to inefficiencies, regional disparities, and periodic stress in repayment cycles.

Nigeria: Risk-Sharing to Enable Participation

Nigeria has introduced risk-sharing mechanisms such as NIRSAL to encourage banks to lend to agriculture. These programs reduce downside risk for lenders, but they do not fully address weak data infrastructure or limited borrower visibility. Lending remains cautious and dependent on institutional support.

Reference: https://nirsal.com/

Thailand: State-Led Agricultural Banking

Thailand’s system is anchored by the Bank for Agriculture and Agricultural Cooperatives. This model has expanded access to rural credit significantly.

However, strong state involvement can reduce incentives for precise risk pricing and may obscure underlying credit risks.

Reference: https://www.baac.or.th/en/

Brazil: Integrated Credit and Insurance

Brazil combines credit, insurance, and government support into a more integrated system. This improves resilience and risk sharing but introduces complexity and can limit accessibility for smaller farmers.

Reference: https://www.worldbank.org/en/topic/agriculture/brief/enabling-the-business-of-agriculture

Comparative Overview of Agricultural Credit Systems

| Dimension | India | Nigeria | Thailand | Brazil |

| Primary Model | Policy-driven lending | Risk-sharing guarantees | State-led banking | Integrated credit + insurance |

| Access | High but uneven | Limited, improving | Broad rural access | Moderate, stronger for large farms |

| Risk Approach | Limited differentiation | Partial via guarantees | State-absorbed risk | Shared risk |

| Data Use | Fragmented | Limited | Moderate | More advanced |

| Key Strength | Scale | Participation | Inclusion | Integration |

| Key Weakness | Inefficiency | Weak fundamentals | Distorted pricing | Complexity |

Despite structural differences, all four systems reveal the same underlying constraint: the inability to accurately measure and price agricultural risk at the farmer level.

The Role of Existing Mechanisms: Partial but Incomplete Solutions

Several mechanisms are widely used to improve agricultural financing outcomes.

Contract farming improves coordination between farmers and buyers but does not eliminate credit risk.

Warehouse receipt loans support post-harvest liquidity but do not address production-stage risk.

Credit guarantees encourage lending but may distort incentives if not paired with strong risk assessment.

Each mechanism addresses part of the problem, but none provides a comprehensive framework for understanding and managing agricultural risk.

The Systemic Outcome: Inefficiency at Scale

The combination of:

- collateral dependence

- weak data infrastructure

- fragmented risk assessment

- unpriced climate exposure

results in a system where:

- productive farmers remain underserved

- risk is inconsistently priced

- financial institutions limit exposure

- supply chains remain fragile

This is not a temporary inefficiency. It is a structural limitation of the current model.

Toward a New Architecture of Agricultural Credit

The limitations of current systems point toward the need for a new approach.

An approach that:

- integrates multiple dimensions of risk

- uses real-time and alternative data

- moves beyond collateral as the primary signal

- aligns credit decisions with production capacity

This shift is explored in detail in:

https://zetarium.com/new-architecture-agricultural-credit-data-driven-risk-models/

Conclusion: From Structural Constraint to Strategic Opportunity

Agricultural finance in emerging markets is constrained not by lack of demand, but by outdated risk frameworks.

The gap between potential and reality remains significant.

Institutions that can better understand and manage agricultural risk will be able to:

- expand lending safely

- improve capital allocation

- strengthen supply chains

- unlock new growth opportunities

The future of agricultural finance will be defined not by the volume of capital deployed, but by the quality of risk intelligence behind it.

Part of a Larger Series

This article is part of a broader thread on credit and risk assessment in agriculture.

👉 Start with the foundation:

The New Architecture of Agricultural Credit: From Scoring to Data-Driven Risk Models

https://zetarium.com/new-architecture-agricultural-credit-data-driven-risk-models/