The New Architecture of Agricultural Credit: From Scoring to Data-Driven Risk Models

Introduction: A Structural Shift in Agricultural Finance

Agricultural finance is entering a structural transition.

For decades, lending to farmers has been anchored in collateral-based risk mitigation. Land, machinery, and physical assets have served as the foundation of credit decisions. While effective in traditional banking models, this approach is increasingly misaligned with the realities of modern agriculture.

Today’s agricultural systems are defined by:

- Climate volatility

- Fragmented production structures

- Contract-based supply chains

- Increasing pressure for sustainability

At the same time, financial institutions are under pressure to expand agricultural portfolios while maintaining capital discipline and regulatory compliance.

This tension is driving a fundamental shift:

from asset-backed lending to data-driven risk assessment

At the core of this transformation lies a critical question:

Can traditional credit scoring and rating systems adequately support modern agricultural finance—or is a new framework required?

Credit Scoring vs Credit Rating: A Structural Limitation

Traditional credit systems fall into two broad categories:

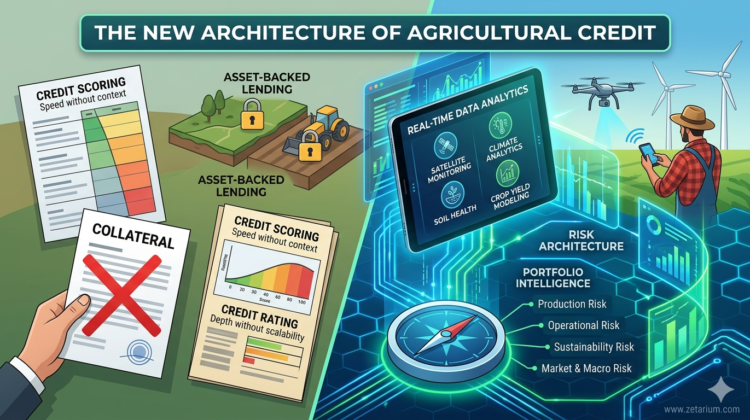

Credit Scoring: Speed Without Context

Credit scoring models provide fast, standardized assessments based on historical financial behavior. They are scalable and efficient, making them suitable for retail and micro-lending environments.

However, in agriculture:

- Cash flows are seasonal and irregular

- External shocks (weather, price volatility) distort repayment patterns

- Historical data often fails to reflect future capacity

This leads to systematic risk misclassification.

Credit Rating: Depth Without Scalability

Credit rating frameworks offer a more comprehensive, forward-looking view by incorporating qualitative and macroeconomic factors.

Yet, they are:

- Time-intensive

- Costly

- Difficult to apply at scale for fragmented agricultural borrowers

The Core Problem: Model Misalignment with Agricultural Reality

The issue is not accuracy alone—it is relevance.

Agriculture is not a standard SME sector. It operates under:

- Biological production cycles

- Environmental dependency

- High exposure to systemic risks

As a result, traditional models—whether score-based or rating-based—fail to capture the true drivers of repayment capacity.

Agriculture Requires a Multi-Dimensional Risk Framework

To address this gap, agricultural credit must be evaluated across multiple dimensions of risk:

1. Production Risk (Land & Environment)

- Soil quality and productivity

- Weather patterns and climate exposure

- Water availability

2. Operational Risk (Farmer Capability)

- Experience and decision-making

- Input management

- Adaptive capacity under stress

3. Sustainability Risk (Long-Term Viability)

- Soil conservation

- Resource efficiency

- Environmental resilience

4. Market & Macro Risk (External Forces)

- Commodity price cycles

- Supply chain dependencies

- Policy and subsidy environments

This layered approach aligns with the systematic thinking behind Zetarium’s framework, as explored in

→ The Four Layers of Agricultural Risk

The Role of Regulation: A Move Toward Internal Risk Accountability

Regulation is accelerating this transformation.

Under evolving frameworks such as Basel 3.1, banks are being pushed away from mechanistic reliance on external credit ratings toward internally justified risk assessments.

Key implications include:

- Mandatory internal due diligence for unrated entities (including most farms)

- Increased scrutiny of risk models and assumptions

- Constraints on capital optimization through internal models (e.g., output floor requirements)

This shift forces institutions to move beyond generic models and adopt context-aware, data-backed methodologies.

In effect, regulation is no longer just a constraint—it is a catalyst for better risk architecture.

From Collateral to Data: The Emergence of Risk Intelligence

The most important shift in agricultural finance is not methodological—it is conceptual.

Historically, lenders asked:

“What assets secure this loan?”

Now, the more relevant question is:

“What is the borrower’s capacity to produce and repay under uncertainty?”

This shift is enabled by the emergence of risk intelligence powered by data.

Modern capabilities include:

- Satellite-based land and crop monitoring

- Climate and weather analytics

- Historical yield modeling

- Behavioral and operational indicators

These inputs transform agricultural lending from a static evaluation process into a dynamic, continuously updated risk assessment system.

This approach also underpins new thinking in pricing and incentives, as discussed in

→ Pricing as a Nudge: Crop Insurance Pricing Strategy

Why Unsecured Agricultural Lending Becomes Viable

Unsecured lending has traditionally been constrained by information asymmetry.

Without collateral, lenders lack visibility into:

- True production capacity

- Operational resilience

- Exposure to external shocks

Data-driven risk models reduce this asymmetry by:

- Improving borrower differentiation

- Identifying hidden low-risk segments

- Enabling risk-based pricing

This allows institutions to move beyond binary approval decisions toward risk-calibrated portfolio construction.

From Loan-Level Decisions to Portfolio Intelligence

Scaling agricultural lending requires a shift from individual credit decisions to portfolio-level risk management.

Key considerations include:

- Geographic concentration (climate exposure)

- Crop diversification (commodity cycles)

- Borrower segmentation (risk distribution)

Institutions that treat agricultural lending as a managed asset class—rather than a fragmented set of exposures—gain a significant advantage.

This perspective aligns with a broader shift in risk thinking, where risk is not merely a constraint but a strategic lever, as highlighted in

→ The Gate and the Compass

Toward a Hybrid Model: Integrating Scoring, Rating, and Data

The future of agricultural credit will not be defined by replacing one model with another.

Instead, it will emerge from integration:

- The speed of scoring models

- The depth of rating methodologies

- The precision of real-time data analytics

This hybrid approach enables:

- Faster decision-making

- More accurate risk differentiation

- Better alignment with agricultural realities

Conclusion: Redefining Creditworthiness in Agriculture

Agricultural finance is moving beyond the limitations of traditional credit paradigms.

Collateral is no longer sufficient.

Historical financial data is no longer decisive.

Static models are no longer adequate.

The emerging architecture is clear:

- Risk must be contextual

- Assessment must be multi-dimensional

- Decisions must be data-driven

For financial institutions, agribusinesses, and investors, this represents more than incremental change—it is a redefinition of creditworthiness itself.

Those who adopt this new framework will not only expand access to capital—but will do so with greater precision, resilience, and long-term profitability.