Sustainable insurance: A Transient Idea or the Inevitable Approach?

Introduction: When Traditional Insurance Hits Its Limits

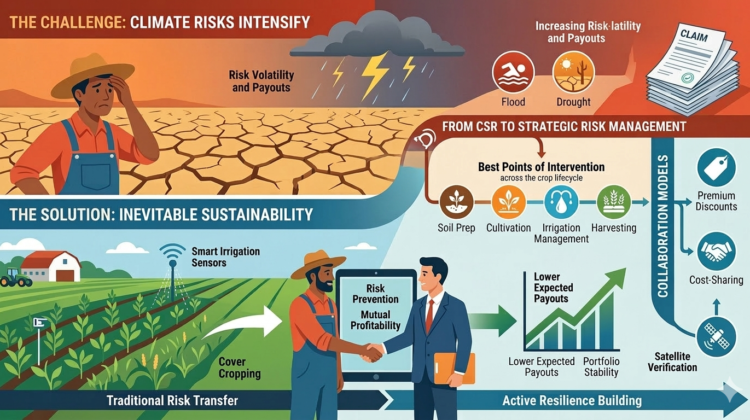

Climate risks are intensifying — and the traditional agricultural insurance model is straining under the pressure. A system built around compensating losses after disasters occur was designed for a more stable world. That world no longer exists.

Insurers face escalating claim volumes. Farmers face growing productivity volatility and financial uncertainty. Neither side wins when every season ends in recovery mode.

The future of sustainable agricultural insurance cannot rest on risk transfer alone. It must shift toward risk prevention — and that shift is not optional. It is inevitable.

This post explores why insurers have strong financial incentives to engage with sustainability, how collaboration with farmers can work in practice, and what data infrastructure makes it all verifiable.

Why Sustainable Agricultural Insurance Makes Financial Sense for Insurers

Sustainability is not a corporate social responsibility exercise. For insurers, engaging with sustainable farming practices is a strategic investment with measurable returns across five dimensions:

1. Lower Expected Payouts

Sustainable practices — including soil health management, efficient irrigation, and crop diversification — directly reduce yield volatility. Lower volatility means lower claim frequency and severity. That improves loss ratios.

2. Portfolio Stability and Supply Chain Security

Insurers who help build stable, productive farming regions protect the agricultural supply chain. This benefits agribusiness clients, food processors, and corporate policyholders downstream. Sustainability, in this sense, is portfolio management at a systems level.

3. Reduced Dependence on Public Subsidies

As insurer portfolios become more resilient, governments face less pressure to step in after failed seasons. Sustainability accelerates post-peril recovery, stabilises policyholders, and reduces incentives for damaging land-use changes.

4. New Products and Revenue Streams

Supporting sustainability opens the door to innovative insurance products — including parametric insurance tied directly to resilience outcomes, value-added advisory services, and cross-selling opportunities that deepen long-term customer relationships.

5. ESG Alignment and Regulatory Readiness

Investors and regulators are demanding ESG alignment at an accelerating pace. Proactive sustainability engagement strengthens capital access, enhances reputational standing, and positions insurers ahead of evolving regulatory frameworks rather than scrambling to catch up.

How Insurers Can Collaborate with Farmers: Four Practical Incentive Models

Punitive mechanisms rarely change behaviour sustainably. Positive financial incentives do. Here are four models that create genuine alignment between insurers and farmers:

|

Model |

Mechanism |

Benefits |

Limitation |

|

Premium Discounts |

Reduced premiums for verifiable sustainable practices (e.g., conservation tillage, water-efficient irrigation) |

Immediate financial motivation |

Discounts alone may not cover large capital investment needs |

|

Cost-Sharing & Co-Financing |

Direct reimbursement or shared financing for infrastructure. Structured as loans, rebates, or milestone-based reimbursements |

Reduces capital barriers · Modernises farm infrastructure · Generates long-term risk reduction |

Needs considerable upfront financing |

|

Resilience & Green Bonds |

Issuing resilience/green bonds · Creating sustainability-linked financing pools · Partnering with capital markets |

Mobilises large-scale funding; leverages insurers’ financial expertise |

Bond structures are complex for individual farmers |

|

Claims Bonuses & Deductible Adjustments |

Reduced deductibles for verified practices · End-of-season resilience bonuses · Higher catastrophe caps for resilience investors |

Rewards long-term low-loss behaviour |

Limited incentive for non-claiming participants unless carefully structured |

|

Why cost-sharing stands out: Insurers are financial institutions. By structuring sustainability investments as bonds, loans, or reinsured programs, they can smooth their own cash flows, incentivise equipment manufacturers to offer farmer financing, and mobilise capital at a scale that premium discounts alone cannot reach. |

Key Intervention Points Across the Crop Lifecycle

Sustainable agricultural insurance is not a single product feature. It is a connected chain of interventions across the entire growing season:

- Before cultivation — Soil mapping, pH correction, nutrient planning, and variety selection matched to local climate conditions.

- Sowing and planting — Lighter machinery to prevent soil compaction, cover cropping, and strategic crop rotation.

- Irrigation and nutrient management — Smart irrigation using sensors and deficit strategies, precision nutrient application, and biological pest control.

- Harvesting — Timely, mechanised harvest that minimises post-field losses.

- Post-harvest — Proper storage conditions, sorting, and cold chain management.

Individual measures work. But they work best as part of an integrated farm resilience program — not as isolated add-ons.

Making It Verifiable: The Data Infrastructure Insurers Need

Incentive systems only function if verification is reliable. Insurers must ensure that sustainability incentives translate into measurable, documented risk reduction. The technology to do this already exists:

- Satellite and remote sensing — for crop health monitoring, NDVI trend analysis, and irrigation pattern verification.

- IoT sensors — soil moisture monitors and on-farm weather stations — for real-time, on-site data.

- Digital farm logs — yield and input records — for outcome measurement over time.

- Third-party certification and audits — where independent validation is required.

|

The practical imperative: define clear KPIs before the season begins, and require verifiable data feeds as a condition of qualifying for discounts or reimbursements. Without this, sustainable insurance programs remain aspirational rather than actuarially sound. |

Conclusion — from CSR to strategic risk management

Sustainable agricultural insurance is not a temporary trend or a rebranding exercise. It represents a structural evolution in how agricultural risk is managed — a shift from passive loss compensation to active resilience architecture.

By combining premium incentives, capital co-investment, innovative financial instruments, and data-driven verification, insurers can reposition themselves as partners in long-term farm productivity — not just payers of last resort.

In doing so, they protect their own underwriting portfolios, stabilise food supply chains, strengthen farmer livelihoods, and reduce systemic dependency on public subsidies.

|

Sustainable insurance is not philanthropy. It is advanced risk engineering for the climate era — and the insurers who recognise that earliest will hold the strongest competitive position as climate volatility continues to rise. |

Read more:

Interested in how parametric structures fit into sustainable insurance programs? Read our post on parametric agriculture insurance →