Bridging the Gap in Agriculture: The Evolution of Parametric Crop Insurance

Introduction: A Coverage Gap That Traditional Insurance Cannot Close

Despite its importance, crop insurance still suffers from low penetration rates compared to other insurance sectors, a shortage particularly evident in developing countries. Traditional methods to increase market share—such as top-down mandates or costly subsidies—are often ineffective. At Zetarium, we believe the solution lies in a new approach: a third-generation parametric framework powered by modern technology.

The Symbiotic Ecosystem: A Win-Win Perspective

To create a robust agricultural market, every policy—from premiums to claim processes—must be designed as a “win-win” for both the insurer and the insured

The Insurer’s Strategic Advantage

The goal for insurers is to shift from reactive loss adjustment to proactive risk management. By utilizing a feedback-loop approach and reliable data, insurers can:

- Propose Fair and Affordable Policies: Lowering the barrier to entry for more farmers and increasing accessibility.

- Expanding the market: more farmers will purchase suitable policies.

- Redistribute Risk: Efficiently compensating losses to sustain the food market, and empower farmers.

- Sustained food market:

- Drive Investment: A stabilized supply side (farmers) attract more investment to promote agriculture industry.

- Bigger agriculture market: bigger market means new customer for insurers and more revenue.

This loop creates a “fortune cycle” of trust, wealth, and sustainability for insurer.

The Farmer’s Path to Resilience

For the farmer, insurance is a tool for growth, not just a safety net. Access to a suitable policy which compensates losses, creates:

- Breaking the Cycle of Misery: Compensation for losses enables farmers to prepare for the next season rather than falling into debt.

- Long-Term Planning: Financial stability allows farmers to enter long-term agreements with food factories and invest more in their operations.

- Expanding the farming business: more stable revenue is the final outcome for the farmer.

Reliable insurance creates a stable financial foundation for the modern farmer.

The Evolutionary Journey of Crop Insurance

Perspective dictates everything. To understand where we are going, we must look at where we have been

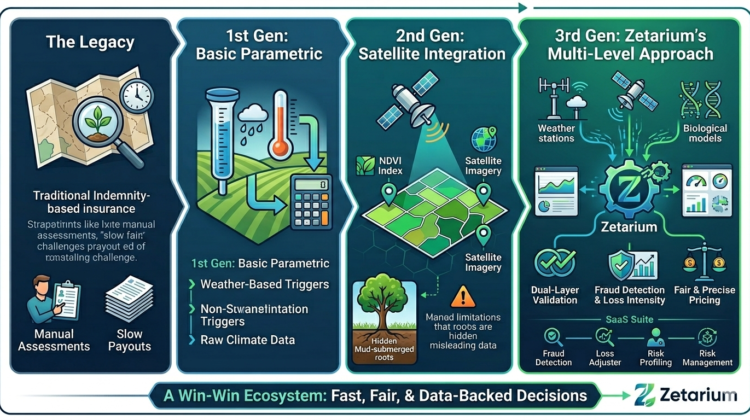

0. The Legacy: Traditional Indemnity-Based Insurance

often antiquated, relying on manual field assessments and excessive paperwork. model is plagued by:

- Human Bias and Lack of Transparency: Subjective assessments lead to disputes.

- Inscalability: Failure to cover remote, vast, or diversified crop fields.

- Systemic Fragility: Catastrophic perils can unbalance portfolios, often leading to insurer default

1. The First Generation: Basic Parametric Indices

The first shift toward innovation was parametric insurance, where payments are triggered by predefined conditions (e.g., rainfall amounts) rather than manual damage inspection. However, early iterations were overly simplistic, relying on raw climate data that lacked local nuance and failed to account for fraud.

2. The Second Generation: Satellite Integration

The introduction of satellite imagery, specifically NDVI (Normalized Difference Vegetation Index), allowed for a more scientific approach to tracking green area to use it for estimating real production.

The Limitation: Satellite data alone can be misleading. For instance, according to a real event, in a flood, a number of fig tree’s crown appeared healthy on a satellite image while its trunk was submerged in mud, leading to certain death. Without considering these complexities, the system lacks true reliability.

The Third Generation: Zetarium’s Multi-Level Approach

We are now on the edge of Third Generation of parametric insurance. This leap forward involves sophisticated mathematical modeling to estimate loss intensity and detect operational fraud.

Our “Small Step” for a Giant Leap

We combine climate-related parameters (traditional First Notice of Loss) with satellite indices (proven claim assessment) to cross-validate results, and considering biological related matters to overcome real challenges. This dual-layer validation provides:

- For Insurers: Protection against “out-of-the-blue” results, reduction in fraud leakage, and prevention of unfair excess indemnity payments.

- For Farmers: Precise risk calculation that removes the need for high markups on premiums, resulting in fairer pricing and reduced default risk.

Our SaaS Suite: Tools for a New Era

To support this vision, Zetarium is building a comprehensive suite of Software as a Service (SaaS) solutions:

| Software | Primary Function |

| Fraud Detection | An automatic system designed to identify fraudulent claims, such as indemnity requests for uncultivated land. |

| Loss Adjuster | A tool that automatically assesses losses based on preset parametric conditions, streamlining the payout process. |

| Risk Profiling | Uses history and gamification to allow users to “sandbox” different scenarios and test policy parameters. |

| Risk Management | A comprehensive Enterprise Risk Management (ERM) software for portfolio estimation and strategic business oversight. |

Conclusion

At Zetarium, we believe in building a more resilient world by reforming how we handle agricultural risk. We serve as the bridge between farmers and insurers, utilizing cutting-edge technology and strategic data expertise to facilitate fast, fair, and data-backed decisions.

By moving beyond simple indices and embracing complex, multi-validated data, we aren’t just selling insurance—we are building the infrastructure for a more resilient agricultural future.