Stop-Loss vs. Excess of Loss: The Future of Agricultural Reinsurance

Introduction: Why Agricultural Reinsurance Is Unlike Any Other Line

Agricultural insurance differs fundamentally from most other lines of insurance due to its high premium levels, frequent catastrophic losses, complex claims assessment, and extreme exposure to climate variability. Severe weather events such as droughts, floods, hailstorms, and heatwaves occur regularly, creating persistent volatility for insurers. These factors define the intrinsic risk profile of crop insurance and agricultural insurance portfolios.

Consequently, reinsurance for agriculture insurance is indispensable for insurers seeking long-term market participation. Selecting the most effective reinsurance structure—particularly between stop-loss reinsurance and excess-of-loss (XoL) reinsurance—plays a critical role in financial sustainability. This article examines key risk management strategies, reinsurance mechanisms, and optimal risk transfer structures to identify best practices for agricultural insurance markets.

Risk Management Methods in Agricultural Insurance

Effective risk management in agricultural insurance typically includes four main strategies: avoidance, mitigation, risk transfer, and acceptance.

1. Risk Avoidance

Due to the high volatility and catastrophic nature of agricultural risks, many insurers avoid entering this market entirely. Climate uncertainty, systemic risk accumulation, and large correlated losses make agriculture one of the most challenging insurance sectors.

2. Risk Mitigation

For insurers active in agriculture, risk mitigation strategies include improved underwriting, farmer compliance verification, loss prevention programs, and enhanced claims validation. However, monitoring farming practices and validating effectiveness of those practices remain operationally complex and cost-intensive.

3. Risk Transfer

Risk transfer through reinsurance emerges as the most effective and scalable strategy. By transferring catastrophic exposures to reinsurers or capital markets, insurers can stabilize cash flow, improve solvency margins, and reduce earnings volatility.

4. Risk Acceptance

For private insurers, full risk acceptance is rarely feasible. However, governments often act as insurers or reinsurers of last resort, absorbing extreme agricultural losses through public disaster relief funds and budgetary support.

Public vs. Private Agricultural Insurance Systems

In many countries, agricultural insurance schemes are publicly subsidized, and governments frequently act as primary insurers or backstop reinsurers. Public entities absorb excess agricultural losses using disaster relief programs and parliamentary funding approvals.

In contrast, commercial insurers rely heavily on reinsurance markets to manage catastrophic agricultural exposures. Global leaders such as Swiss Re, Munich Re, and Hannover Re provide critical reinsurance capacity, enhancing market stability, underwriting sustainability, and financial resilience.

Risk Transfer Mechanisms in Agriculture

Several risk transfer mechanisms exist for managing agricultural risk:

1. Reinsurance

Agricultural reinsurance remains the dominant risk transfer solution. Insurers give part of their underwriting exposure to reinsurers, allowing risk diversification, capital relief, and protection against catastrophic losses.

2. Coinsurance

Historically, merchants pooled risk during maritime transport by jointly insuring cargo shipments. In contemporary insurance markets, co-insurance involves multiple insurers jointly underwriting a single policy, each assuming a predetermined share of premium and claims. This approach spreads risk but does not eliminate exposure to systemic catastrophic events.

3. Catastrophe Bonds (Cat Bonds) and Insurance-Linked Securities

Modern financial instruments such as catastrophe bonds and weather derivatives allow insurers and reinsurers to transfer agricultural catastrophe risk directly to capital markets. These insurance-linked securities (ILS) enhance market capacity, reduce reliance on traditional reinsurance, and improve pricing efficiency.

Reinsurance Structures: Proportional vs. Non-Proportional

Reinsurance arrangements typically fall into three categories:

1. Facultative Reinsurance

Facultative treaties are negotiated on a case-by-case basis and are not scalable for large agricultural portfolios.

2. Proportional Reinsurance (Quota Share)

Under quota-share reinsurance, reinsurers assume a fixed percentage of premiums and claims. This structure promotes operational collaboration, technical support, and underwriting discipline, making it suitable for emerging agricultural insurance markets.

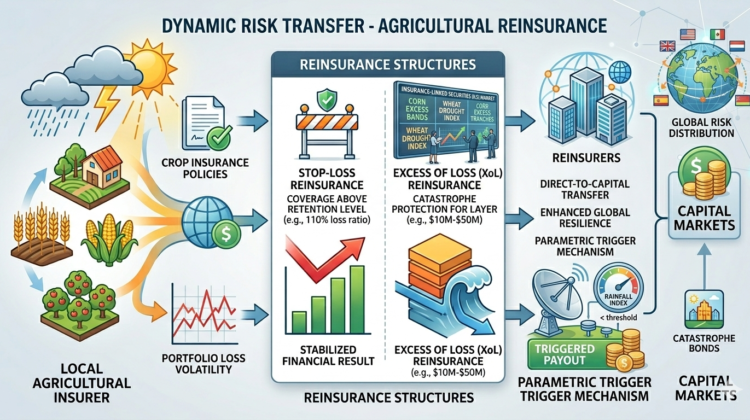

3. Non-Proportional Reinsurance (Excess of Loss & Stop Loss)

Excess-of-loss (XoL) reinsurance, including stop-loss arrangements, provides coverage once losses exceed predefined retention levels. This structure is particularly effective for catastrophic agricultural risk management and is widely used in crop insurance and parametric insurance portfolios.

Insurer Perspective: Quota Share vs. Excess of Loss

From an insurer’s perspective, quota-share reinsurance offers operational advantages through close collaboration with reinsurers, enhanced underwriting quality, and improved claims management. In reality, insurer, reinsurer and insuring process are evolved during this process.

However, excess-of-loss reinsurance provides superior catastrophe protection. Although insurers relinquish part of premium income, XoL treaties dramatically reduce loss volatility, insolvency risk, and capital strain. This leads to greater financial resilience, solvency stability, and regulatory capital efficiency, especially in climate-sensitive regions.

Reinsurer Perspective: Risk, Return, and Capital Accumulation

From a reinsurer’s perspective, agricultural excess-of-loss treaties present both high return potential and elevated volatility risk. Although catastrophic agricultural losses are theoretically low-frequency, climate change has increased the recurrence of extreme events.

Retained premiums enable reinsurers to accumulate capital and generate compounded investment returns. However, reinsurers also face significant accumulation risk, especially across geographically correlated agricultural portfolios.

Fortunately, agricultural risks exhibit stabilizing features, including seasonality, bounded peril windows, and predictable production cycles. These characteristics allow reinsurers to model exposures accurately, optimize retention thresholds, and recalibrate pricing annually.

The Strategic Importance of Excess of Loss Reinsurance

Excess-of-loss reinsurance remains the cornerstone of catastrophic agricultural risk management. Its integration with catastrophe bonds and capital market instruments enhances global risk distribution and strengthens systemic resilience.

However, XoL structures require sophisticated actuarial modeling, high-quality data, and reliable claims validation frameworks. In traditional indemnity-based insurance, uncleared claim verification increase uncertainty and capital lockup. In the worst case, there is risk of irresponsibility of main insurer when it doesn’t adjust losses and approves all claim for payment. Without robust claims infrastructure, quota-share arrangements may provide safer alternatives.

By contrast, parametric agricultural insurance, where payouts are triggered by objective indices such as rainfall, temperature, or satellite-based yield estimates, offers superior transparency, faster settlements, and lower operational costs. Parametric approach naturally is cleared and significantly improves excess-of-loss design, reduces basis risk, and enhances capital efficiency for reinsurers.

Conclusion: The Future of Agricultural Reinsurance

The future of agricultural reinsurance lies in excess-of-loss structures supported by parametric triggers, advanced climate modeling, and capital market integration through catastrophe bonds and ILS.

As climate change intensifies systemic agricultural risk, the combination of data-driven reinsurance design and parametric insurance infrastructure will become the essential foundation of sustainable agricultural insurance ecosystems — for insurers, reinsurers, and ultimately for the farmers and food systems they exist to protect.

The structural choice between stop-loss and XoL is not purely technical. It reflects a strategic decision about how an insurer manages volatility, capital, and the long-term relationship with their reinsurance partners. Getting that choice right — and pairing it with the right data infrastructure — is what separates insurers who thrive across market cycles from those who exit after the first bad season.

|

The future of agricultural reinsurance is not just about structure — it is about data quality, parametric clarity, and the infrastructure that makes fast, fair, and verifiable settlements possible at scale. |